Introduction

Are you a foreigner doing business in the United States? Navigating the U.S. system may be tricky. If you’re generating effectively connected income (ECI), you may have an obligation to report and pay taxes on such income to the Internal Revenue Service.

Understanding ECI may reduce stress during the tax season and help you avoid future issues. This comprehensive guide outlines the basics you need to know about ECI.

What is Effectively Connected Income (ECI)?

When a foreign person is engaged in a trade or business in the United States, income related to that business is likely to fall under Effectively Connected Income (ECI). In simple terms, ECI could be the income you earn from actively doing business in the United States, unless otherwise a treaty applies.

This concept is particularly relevant for foreign individuals and entities engaged in business activities in the U.S., as it determines their tax obligations.

Example:

Sarah, a German citizen and non-U.S. tax resident, owns a restaurant in Chicago while living in Germany. Her restaurant business in the United States brings in $200,000 a year, while her stock investments in Germany bring in $20,000. Since the $200,000 restaurant revenue is actively generated through a U.S. business, it is likely to be classified as ECI. However, the $20,000 in investment income from Germany is unlikely to be ECI, as it has no connection to U.S. operations. So, this $20,000 earned in Germany is unlikely to be taxed in the U.S.

Now, let’s discuss the tax treaty implications on ECI in the next section.

U.S. Tax Treaty Impact on ECI

If a foreign person has effectively connected income (ECI), U.S. domestic tax law generally allows the IRS to tax it. However, a tax treaty may change this outcome. Generally, most U.S. tax treaties include the concept of a “permanent establishment” (PE). Under these rules, the U.S. may tax a foreign person’s business profits likely if the foreign person has a PE in the United States. When a treaty applies, its rules generally override the domestic ECI rules.

This is why the treaty may limit or even eliminate U.S. tax on effectively connected income that would otherwise may be taxed under domestic law.

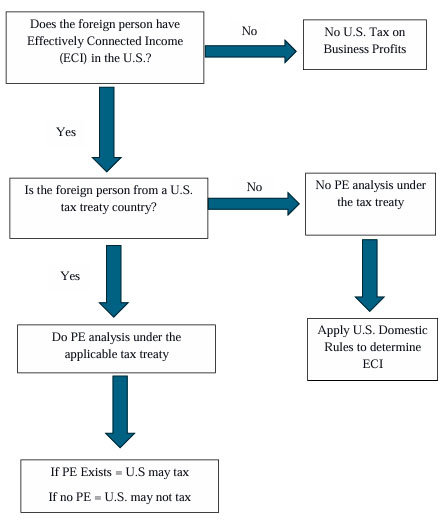

Flowchart to illustrate the Impact of the Tax Treaty on ECI

Let’s break down how this works through the following flowchart:

The following flowchart demonstrates that a foreign person is taxed in the U.S. on business income if it is considered Effectively Connected Income (ECI). Once ECI exists, the next step is to check whether the person is from a tax treaty country. If a treaty applies, then one should do a Permanent establishment (PE) analysis. Here, the U.S. may tax the income likely when a PE exists. If no treaty applies, the U.S. relies solely on domestic U.S. tax rules to determine ECI.

Example: Under Article 7(1) of the US-UK tax treaty, the U.S. may tax the U.S. portion of business profits of a UK Company only if the UK Company has a permanent establishment in the United States.

Suppose a UK firm provides certain services to U.S. customers.

Under the US–UK tax treaty, the U.S. may tax business profits only if the firm has a permanent establishment (PE) in the United States. Let’s assume that the firm does not meet the PE conditions under the tax treaty. So, even if the UK firm generates ECI under U.S. domestic law, it is unlikely to be taxed in the U.S. because it does not qualify as a PE under the tax treaty. It is evident that the treaty overrides domestic law, and the U.S. is unlikely to tax the consulting profits.

Determining ECI in the absence of a U.S. Tax Treaty

Let’s assume that there is no tax treaty between the US and the UK in the above example. In that case, there is no concept of permanent establishment without a tax treaty. Therefore, one should analyze the U.S. domestic rule on determining whether the business profits constitute ECI. Under U.S. domestic law, the business profits from such activities may be classified as Effectively Connected Income (ECI) if the activities are considered a U.S. trade or business.

In the above example, if the UK firm performs activities that constitute U.S. trade or business, the business profits from those activities may be classified as ECI. As a result, the U.S. may tax such profits.

Next, let’s understand what a U.S. Trade or business that eventually leads to ECI in the next section is.

What is a U.S. Trade or Business?

United States trade or business (USTB) is generally defined as a foreign person or company engaging in trade or business within the United States. Such trade or business could be activities generating income from performing services or selling goods.

For instance, when a foreign person performs personal services in the United States, they are typically engaged in a U.S. trade or business, with certain exceptions.

Also, when a foreigner operating a business in the U.S. that sells services, products, or merchandise is engaged in a trade or business in the U.S., with certain exceptions.

For example, if a foreign company opens and operates a clothing store in the U.S., it actively sells products from a physical location in the U.S. As a result, this company is considered to be engaged in U.S. trade or business.

Next, let’s talk about what income qualifies as ECI.

What Income Qualifies as Effectively Connected with a U.S. Trade or Business?

Income is “effectively connected” to a U.S. trade or business (USTB) based on the following factors:

Tax Status

First, it is essential to verify that the recipient of the income is either a Nonresident alien (NRA) or a foreign corporation. This is because such foreign persons are qualified to generate ECI.

In the next section, we will discuss the importance of US trade or business in generating ECI.

Engagement in a U.S. Trade or Business (USTB)

Secondly, it is essential to evaluate whether the foreign person is actively engaged in a trade or business in the United States , which generally depends on the nature of the foreign person’s activities. Such activities may include conducting personal or professional services in the United States or selling products or merchandise in the USA.

For example, a foreign company opens and operates a clothing store in the U.S., actively selling merchandise through a physical location. In that case, the company is engaged in a U.S. trade or business.

Income Source Rules for Determining ECI

Generally, ECI includes U.S.-source income effectively connected with a trade or business in the United States. The following two categories of U.S. source income may qualify as effectively connected income (ECI):

- Certain Types of Fixed, Determinable, Annual, or Periodical (FDAP) Income

- All Other U.S.-Source Income

Let us understand them in detail in the following section:

1. Certain Types of Fixed, Determinable, Annual, or Periodical (FDAP) Income:

FDAP stands for fixed, determinable, annual, and periodical income, which includes income that is fixed or otherwise determinable, and is paid annually or periodically at irregular intervals. FDAP Income generally includes interest, dividends, rents, and royalties.

However, not all FDAP income is considered “effectively connected income” (ECI). For instance, passive income, such as dividends from owning stock in a U.S. company without engaging in business activities, is excluded from ECI.

In specific circumstances, FDAP income may qualify as ECI. The IRS generally uses two key tests to determine this:

- Asset-Use Test: This test looks at whether your assets are used in your U.S. business. If the income is derived from assets tied to your U.S. operations, it may qualify as ECI. Example: Let’s say you operate a vineyard in California and rent out part of the land to a local distributor. The rental income from this property is directly linked to your vineyard business. In that case, it could qualify as ECI.

- Business Activities Test: This test examines whether your U.S. business activities played a significant role in generating income (even if it is passive in nature). If your U.S. operations contributed to earning the passive revenue, it could be considered ECI. Example: Maria, a Spanish entrepreneur, has a U.S.-based office. From this office, she actively manages and negotiates patent agreements for her licensing business. The royalties she earns from U.S. companies are derived from her active U.S. business and qualify as ECI, likely subject to U.S. tax.

2. All Other U.S.-Source Income: If a foreign person is engaged in a U.S. trade or business (USTB), most of their S. source income is likely to be treated as effectively connected income (ECI).

Relevant facts and circumstances may dictate the resulting conclusion when determining whether someone is engaged in a U.S. trade or business. The following are examples of situations where a foreigner may be considered connected with a trade or business in the U.S., and ECI would exist:

- Running a partnership that does business in the U.S.

- Managing your own LLC in the U.S.

- Providing services while physically present in the U.S.

- Selling products or services to U.S. customers via owning and operating a business in the U.S. For example, Jin is a Korean individual who owns and operates a clothing store in Los Angeles, making $300,000 in sales. Since he’s running the business in the U.S., this income is likely classified as ECI and taxable in the United States. When a foreign person sells U.S. real estate property, the gain or loss may be treated as ECI.

- If you are temporarily in the United States on an F, J, Q, or M visa, any taxable portion of a U.S.-sourced scholarship or fellowship grant you receive will be considered effectively connected with a U.S. trade or business.

However, if your only U.S. business activity is trading stocks, securities, or commodities through a U.S. broker, then any income from that may not be considered ECI.

Foreign-source income is generally not treated as ECI unless it’s attributable to a U.S. office or fixed place of business (with limited exceptions).

U.S. Tax Implications of ECI

If income is effectively connected with a U.S. trade or business, then the foreign person’s taxable income is computed similarly to that of U.S. persons. The following could be the tax consequences on the ECI Income:

- You’ll likely pay taxes at graduated rates on a net basis, just like U.S. citizens.

- You may deduct your business expenses and specific itemized deductions.

- You’ll need to file either Form 1040-NR (for individuals) or Form 1120-F (for corporations).

- Foreign persons who don’t report ECI may face some penalties, including the following: failure to file, failure to pay, accuracy-related penalties, and interest on unpaid taxes. Willful evasion may result in criminal prosecution, with significant fines and imprisonment.

Conclusion

For foreign individuals and businesses operating within the U.S., understanding effectively connected income is essential, as it directly impacts their tax obligations and compliance requirements. Foreign taxpayers may effectively manage their obligations under U.S. tax law by understanding what ECI is and how it is taxed.

Are you looking for personalized advice on how to handle your Effectively Connected Income (ECI) tax obligations in the United States? Contact the International Tax Attorney at Arora Law P.C. today at (201) 620-1482 for an international tax consultation.

Disclaimer: The information provided in this article is for general informational purposes only and does not include legal advice. This article does not comprise an attorney-client relationship between the reader and Arora Law P.C. or its attorneys. If you have specific questions regarding your individual situation, please consult with a licensed attorney.

The information in this article is current as of the publication date. U.S. Tax laws and regulations change frequently, and readers should confirm whether any updates have occurred since.